What is a Deposit Insurance Corporation?

The Deposit Insurance Corporation (LPS) is an institution that was formed independently based on Law No. 24 of 2004 and was later renewed by Law No. 7 of 2009, which discusses the Deposit Insurance Corporation or the LPS Law.

Fundamentally, the deposit insurance corporation is an improvement over the government guarantee program that was previously in effect in the form of a blanket guarantee valid from 1998 to 2005.

Why is a Deposit Insurance Corporation needed?

Previously, the blanket guarantee was successful as one of the factors that increased public trust in banks. The blanket guarantee is a temporary measure carried out during emergencies such as a systemic crisis in the banking sector.

The blanket guarantee aims to reduce the runaway of deposits and restore public confidence in the banking system. LPS or deposit insurance institutions are also expected to do the same with blanket guarantees.

However, it should also be noted that a blanket guarantee is a policy that burdens state finances and creates a moral hazard impact on banking actors and customers, as stated on the LPS official page. For this reason, the policy was officially terminated in 2005.

For this reason, the Deposit Insurance Corporation hopes to improve policies that burden the country's finances without reducing public confidence in banks.

Functions of the Deposit Insurance Corporation (LPS)

From an explanation of the background and reasons for its existence, there are at least two functions of the Deposit Insurance Corporation (LPS):

- Guaranteeing customer deposits.

- Guaranteeing insurance policies.

- Actively participating in maintaining the stability of the banking system in accordance with its authority.

- Carrying out bank resolutions.

- Resolving problems of insurance companies and sharia insurance companies whose business licenses have been revoked by the Financial Services Authority (OJK).

Duties of the Deposit Insurance Agency (LPS)

There are at least 9 duties of the deposit insurance agency (LPS), which are listed on the official LPS website:

- Formulate and determine the policy for implementing deposit guarantees.

- Implement deposit guarantees.

- Formulate and determine the policy for implementing policy guarantee programs.

- Implement policy guarantee programs.

- Formulate, determine, and implement financial system stability policies in accordance with its authority.

- Formulate, determine, and implement preparations for bank resolution actions, including due diligence on banks and exploration of other banks or investors.

- Formulate, determine, and implement bank resolution policies designated as Banks Under Resolution.

- Formulate, determine, and implement preparations for the liquidation of Insurance Companies and Sharia Insurance Companies.

- Formulate, determine, and implement liquidation policies for Insurance Companies and Sharia Insurance Companies whose business licenses have been revoked by the OJK.

Authority of the Deposit Insurance Corporation (LPS)

LPS has several authorities in its functions and duties as an institution established under law.

- Determine and collect insurance premiums and periodic insurance contributions for policies.

- Determine and collect contributions when banks first become participants and initial contributions when insurance companies and sharia insurance companies first become participants.

- Manage LPS assets and liabilities, including writing off and writing off assets in the form of receivables and other assets.

- Obtain data on savings from depositors, bank health data, bank financial reports, and bank audit reports.

- Obtain data on policyholders, insured, and insurance participants, health data for insurance companies and sharia insurance companies, financial reports for insurance companies and sharia insurance companies, and reports from insurance companies and sharia insurance companies.

- Conduct reconciliation, verification, and/or confirmation of the data in points 4 and 5.

- Determine the terms, procedures, and provisions for payment of insurance claims and implementation of policy guarantees.

- Appoint, authorize, and/or assign other parties to act for the interests and/or on behalf of LPS, in order to carry out certain tasks.

- Conducting counseling to banks, insurance companies and sharia insurance companies, as well as the public regarding deposit guarantees and policy guarantees.

- Conducting bank inspections both independently and together with the OJK.

- Placing funds in banks under recovery based on requests from the OJK.

- Appointing statutory managers at banks that receive fund placements from the LPS.

- Transferring insurance portfolios, paying guarantee claims, and returning premiums for contributions that have not been made when insurance companies and sharia insurance companies are liquidated.

- Transferring insurance policies without the consent of insurance policyholders.

- Imposing administrative sanctions.

Terms of Guarantee for the Deposit Insurance Corporation

Several guaranteed requirements for the Deposit Insurance Corporation must be met, as listed on the official LPS website. Among others:

1. All bank books are properly recorded

The first thing that becomes a guaranteed requirement for a deposit insurance institution is proper bank records and bookkeeping. In this case, personal data and customer lists must be detailed in the bank's books. In addition, all evidence of banking transactions must also be stored properly.

2. The interest rate received by the customer does not exceed the LPS guarantee interest rate

Customers who make deposits at a bank are not allowed to benefit from the bank where the customer has unusually deposited their money. One of the advantages that can be obtained unusually is obtaining an interest rate that is unreasonable or exceeds the maximum guaranteed interest rate set by LPS.

LPS also advises and reminds a customer of a bank not to be tempted and to always act wisely with cashback from the bank.

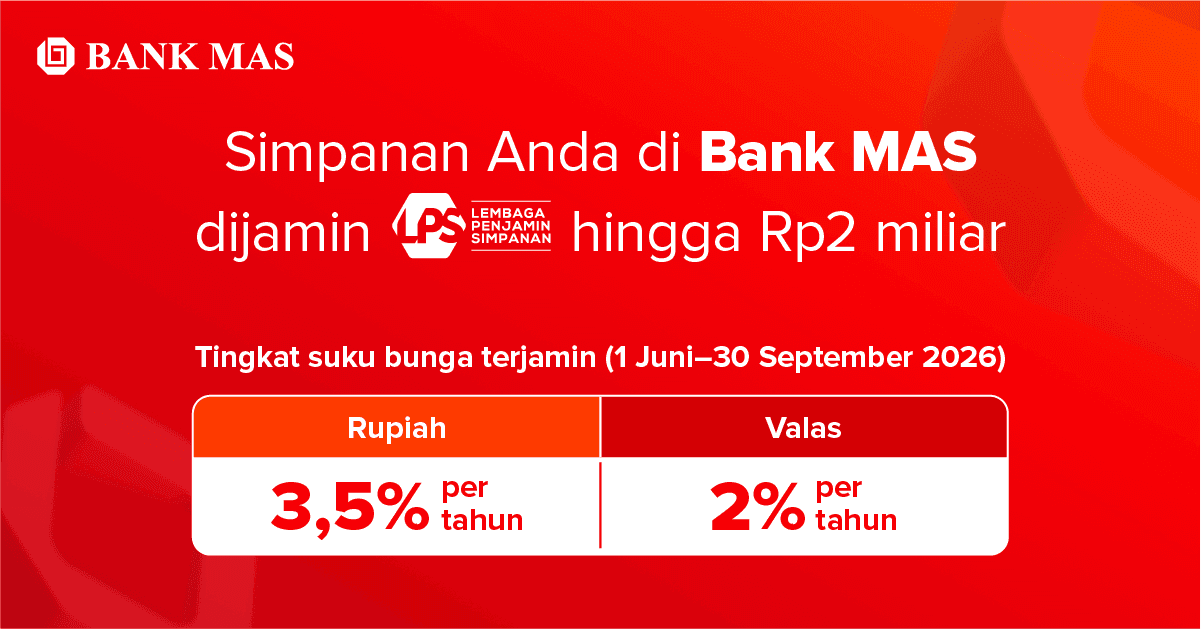

According to the LPS official website, the guaranteed interest rate for 1 June 2026 - 30 September 2026 is as follows:

a. Rupiah interest rate 3.5% p.a

b. Forex interest rate 2% p.a

3. Do not take actions that can harm the bank.

Several actions taken by customers can be one of the leading causes of a bank experiencing losses. These actions include bad credit and other delayed payments that make the bank's condition unhealthy or stable.

Generally, the LPS guarantee requirements above are known as 3T, are well recorded, the interest rate does not exceed the maximum limit, and does not harm the bank.

If the 3T is carried out correctly, then the savings owned by a customer can be guaranteed by the Deposit Insurance Corporation or LPS. In addition, customers have no fees deferred to obtain guarantees from LPS because deferred fees to customers have become the bank's responsibility where the customer's deposits are stored.

What is the deposit value guaranteed by LPS?

Starting on October 13, 2008, the LPS has determined that the maximum deposit value that the Deposit Insurance Corporation can guarantee is IDR 2 billion for one customer at a bank, as stated in Article PP 66 of 2008 regarding guaranteed value. .

This means that if a person has multiple accounts at a bank, then the amount of the guaranteed balance is the accumulation of all accounts at that bank. According to the stipulation, the value that can be guaranteed is only IDR 2 billion.

Details of the value of the guaranteed deposit at the LPS are the principal amount of the deposit plus interest for those who save at conventional banks or profit sharing for those who keep at Islamic banks.

So, what if customer deposits are more than IDR 2 billion?

For customers who have savings above IDR 2 billion, it will be the authority of the liquidation team based on the liquidation results of the bank's assets.

Claim payment procedures to LPS storage customers

1. Verification process

Verifying is the first process of determining which deposit customers are eligible for payment. LPS will look again at the customer's deposit that submitted the claim to decide whether or not it has received deposit guarantee payments.

The verification process for customer data entitled to a deposit from LPS lasts 90 working days from when the bank's business license is revoked.

2. Deposit payment process

After the verification and reconciliation process for the bank customer's deposit data is deemed safe, LPS will pay deposit guarantees to the customer five working days after the verification process for the bank whose business license has been revoked begins.

3. Timeframe for filing a claim

LPS provides a period of filing a guarantee claim for five years after the business license of the bank where the customer makes deposits is revoked.

Bank MAS is one of the banks registered with the Deposit Insurance Agency or LPS. This, of course, will make you more secure in carrying out saving activities at Bank MAS.

That is a complete explanation of LPS. So, ensure you save your money in a bank that has joined the LPS and follows the LPS regulations to keep your money safe. You can visit the LPS FAQ page if there are some things you still need help understanding